To nobody’s surprise, the US and Iran are back at war. After Washington launched a new series of strikes on Iran on July 8th, the two are exchanging fire on assets across the Gulf. Once again, movement through the Strait of Hormuz, the world’s major thoroughfare of oil exports, is minimal and global fuel prices are creeping back up.

North Africa, still reeling from the consequences of the fighting earlier this year, is nervously watching on. Egypt’s and Tunisia’s finances are suffering and the balance of power between Morocco and Algeria looks shaky, as does Libya’s delicately poised political status quo. The war’s corrosiveness is pushing the region closer to instability. This was true after the ceasefire, and even moreso now it has been broken.

For Europe, north Africa’s travails are a security and economic threat. But they are also an opportunity for Europeans to finally redevelop their relations with their southern neighbours by helping buttress them against this tumultuous new world and in turn, protect themselves against future unrest.

Taking blows

As import-oriented economies, North African countries are largely dependent on streams of global currencies, and they are increasingly energy hungry. This makes them hyper vulnerable to the Iran war’s geopolitical and geoeconomic fallout, as the first wave of fighting made all too clear.

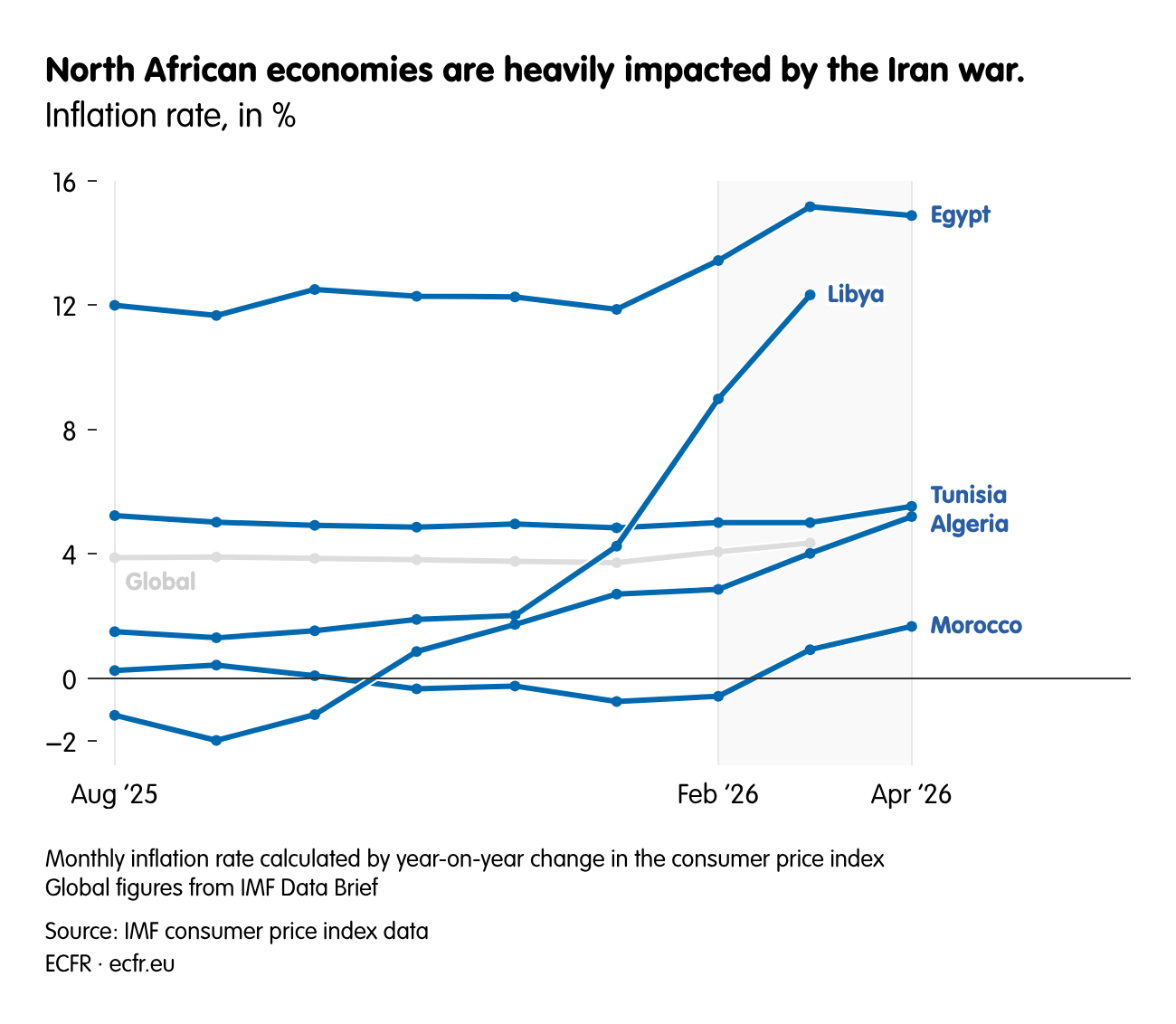

When Iran closed the strait of Hormuz in February and struck energy terminals across Arab gulf states, it hit energy markets and upended budgets across the region. The Tunisian government, for example, already locked in a Sisyphean struggle to find enough foreign currency for key monthly imports and loan repayments, designed their budget with an assumed price of oil at $63 per barrel, only to see it soar to over $100. They almost depleted their emergency reserve within the first few weeks of the war and relied on quiet energy loans from neighbours. Egypt, similarly, was forced to go to Libya and costly spot markets after Israel declared force majeure on key gas exports following the gulf shutdown. The government even forced 24-hr metropolises into darkness after 9pm. The region now faces this new round of fighting with the energy stores depleted and the coffers dry.

North Africa’s oil economies were also affected. Algerian and Libyan hopes to leverage high oil prices have been stymied by loans to neighbours, production limits and domestic energy demands. Libya—which depends on fuel imports and suffers from massive fuel smuggling operations—had their first unified budget in years gravely unbalanced before even being signed.

It is not just energy. Exports of two seemingly innocuous chemicals, urea and sulphur, have also been hit, crippling a fertiliser industry central to north African economies (and food supply). Morocco is home to the world’s largest phosphate exporter, while Egypt, is one of the world’s largest consumers and exporters of fertilizer. Tunisia’s phosphate industry is a jewel of its economy, yet entirely dependent on imported materials. As a region that imports over half its food, the falling export revenues and raised costs of domestic agriculture are acutely painful. Government costs are rising, labour-intensive industries contracting, exports falling, while the prices of basic foodstuffs inflate in a region where food insecurity already doubled between 2019 and 2024.

The long-term damage

North Africa’s longer-term struggle will be maintaining the foreign currency streams that fund imports and, by extension, social programmes. In other words, the war has triggered consequences that will become new structural realities

After the shock of these initial blows, North Africa’s longer-term struggle will be maintaining the foreign currency streams that fund imports and, by extension, social programmes. In other words, the war has triggered consequences that will become new structural realities.

As calm returned following the initial ceasefire, energy, fertiliser, food, tourism and shipping markets began returning to normal. This gave regional governments some clarity over cashflows. And, with the diplomatic structures from the ceasefire in place, markets are proving slightly more resilient following the recent outbreak of violence. However, the renewed war is still young and the future ominous. For North Africa’s two largest foreign currency streams—remittances and Arab gulf investments—the omens are even worse, leaving the region in crippling suspense over what comes next.

The Gulf is north Africa’s main labour market, especially for Egypt which has 3.3 million nationals in the region. Remittances from this labour are a vital stabiliser for the region’s poorer economies, with increasing importance during tough times as a forex supply and economic ballast that governments do not have to pay for.

Last year, the value of remittances to Morocco was around €11.4bn, roughly 8% of GDP; it is already 10% higher so far this year. In Tunisia it was €2.6bn, 5.6% of GDP but making up around 30% of Tunis’s foreign currency reserves. In Egypt the statistics are even more concerning as remittances grew a startling 40.5% year-on-year to €36.2bn, roughly 12% of GDP.

The Gulf is also the largest source of foreign investment. It has repeatedly bailed out Egypt, provided a rare source of foreign projects in Tunisia’s otherwise seized economy, and in Morocco, the UAE alone accounts for 19% of foreign direct investment.

Given the scale of dependence, even small constrictions in Gulf labour markets and investments could destabilise these economies through hitting remittances and GDP respectively. Among North African capitals, there is a deep-seated fear that Gulf economies are much harder hit than let on, with anecdotal expectations of mass layoffs and cuts to foreign spending.

Instability ahead

This is a grim forecast for already suffering economies with simmering unrest. Poor finances have fuelled a long-running battle between Tunisia’s government and protestors while 2025 saw Morocco’s worst protesting since 2011’s Arab Spring. In the shadow of the Iran war, cost-of-living and inequality issues will only worsen. Similar anxieties drove Egyptian president Abdel Fattah el-Sisi to send air-defence systems to the Gulf and visit Abu Dhabi, to shore up the relationship after the UAE expelled thousands of Pakistani labourers seemingly as punishment for Islamabad’s diplomatic efforts.

Amid it all, the rivalry between Algeria and Morocco has intensified. Thanks to the energy crisis, Algiers leveraged high oil prices to: accelerate energy-sector development; consolidate its trilateral Maghreb union (that pointedly excludes Morocco); court Europe with energy; and advance the trans-sahara pipeline linking Nigerian and Nigerien oil to Algeria’s export terminals.

This has toppled the regional balance of power in Algiers’s favour, just as Rabat’s closest allies—the US, the UAE and Israel—are otherwise occupied. As their pantomime rivalry is the pivot on which regional stability and politics rests—especially given their spiralling arms race—this misbalancing could lead to heightened tensions and other flashpoints throughout the region most notably over the Western Sahara.

In Libya, high oil prices enticed Turkey and the US to try and use the lure of energy sector developments and the potential for profiting off them as bait for a new political agreement. Unsurprisingly, this has only stoked mass protests from a population long-promised elections and struggling with the worst cost-of-living crisis since the 1950s because of the kleptocracies this deal is trying to unite.

Fertile ground for Europe

As the region’s political economy teeters on the edge, it might seem that there is little Europe can do to stop a cascade of instability it was never really involved in. But at the precipice of crisis is also a platform for Europe to advance its strategy to transform relationships with North Africa, most recently articulated in the EU’s pact for the Mediterranean. Given the pact’s purpose is to redevelop Europe’s southern relations and build closer working partnerships, there is no better moment to see it through. After all, a friend in need is a friend indeed.

Both the EU and its member states can help stabilise the situation and in turn, improve relations. Interested countries, like Spain, France and Italy could donate or cheaply loan their Special Drawing Rights—an asset provided by the IMF designed to supplement a state’s foreign exchange reserves—to ensure struggling regional economies ride out the storm. Alongside this they should encourage the European Commission to extend the food and resilience facility for the southern neighbourhood to help struggling states deal with the fallout of the fertiliser crisis.

Such steps would help Europeans develop credibility and good will, stabilise the neighbourhood and lay the groundwork for expanded EU engagement in north Africa. The commission could then build on this in the long-term by going to regional capitals with plans to develop green power generation, facilitate European private-sector investment, and develop infrastructure through Global Gateway. This would satisfy the region’s energy and economic imperatives while developing the green energy imports and nearshoring environment that Europe needs.

After a year of unrest, North Africa may very well stabilise itself, but there is a decent chance it could deteriorate into polycrisis. Regardless of the outcome, if Europe refuses to respond it will once again be assuming the position of the passive bystander, the worst geopolitical role possible at a time of either great opportunity or dire crisis.

The European Council on Foreign Relations does not take collective positions. ECFR publications only represent the views of their individual authors.